Global bond yielding less than zero (yes, that means lenders are paying the Government to let them hold their paper) now exceed 8 Trillion dollars. In total, there are 18 countries with negative bond yields ... in the 10th year of one of the largest global economic expansions no less.

Central banks only tool left in their toolbox in an attempt to counter slow or negative growth is to stimulate the economy by lowering interest rates. At some point all that want to borrow have done so and keeping rates so low harm only those who require bond income (retirees). With this going on since the 2008-09 crash and not having the desired effect one has to wonder why continue and then immediately brings to mind this quote

The definition of insanity is doing the same thing over and over again, but expecting different results – Albert Einstein

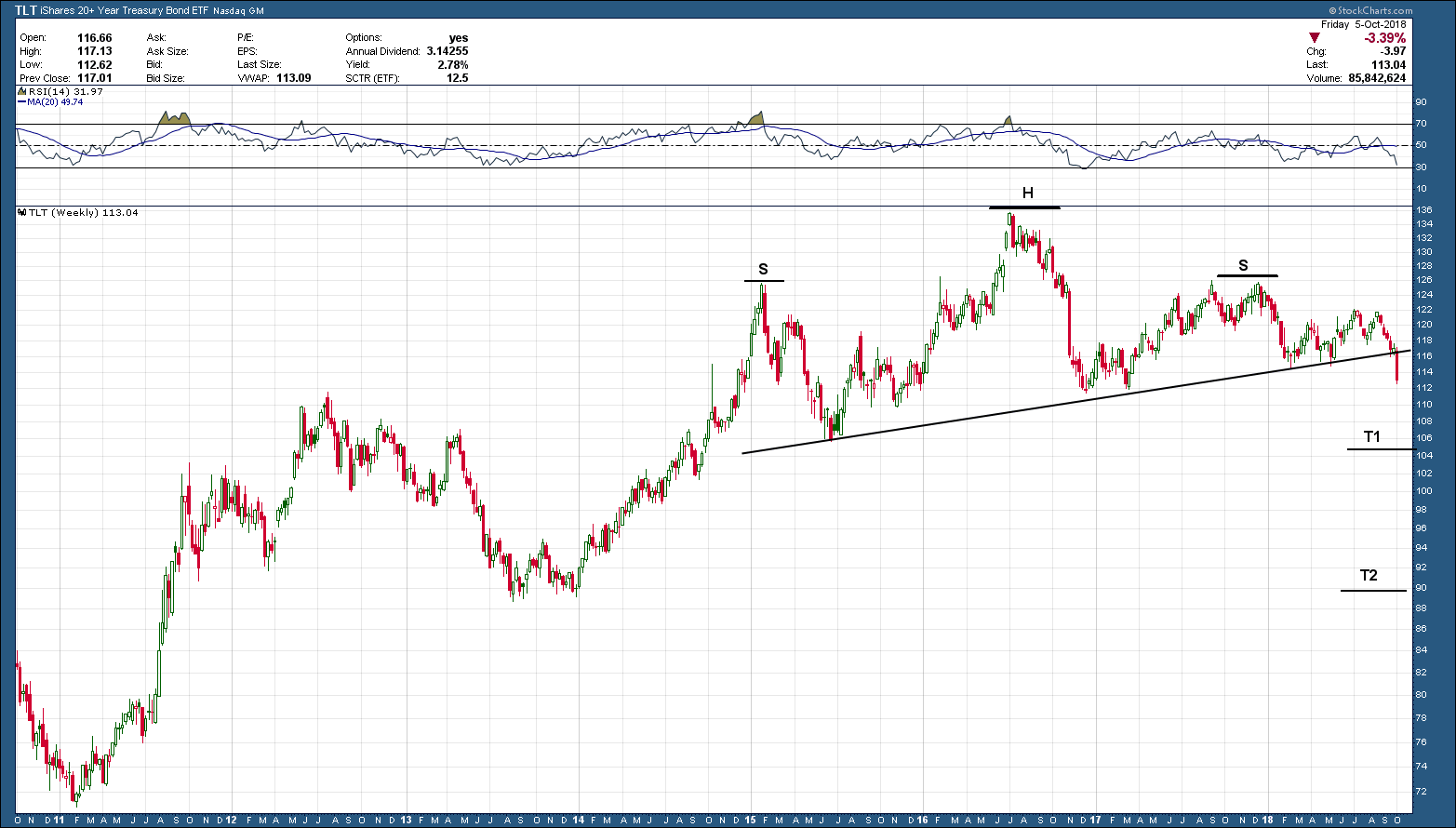

You need to look no further than the chart above to the reason why I am a firm believer Europe is winning the race …… to the bottom and the next economic crisis will begin from that region of the world.