Check it out and let me know what you think. Did Marc Faber's call have you exit stocks or do you think there is more upside?

Have a great week everybody

INVESTMENT EDGE

Check it out and let me know what you think. Did Marc Faber's call have you exit stocks or do you think there is more upside?

Have a great week everybody

You’ve heard it over and over again and I can tell you first hand that its true ... The trend is your friend. While we have all heard it before what does it really mean? As a trend following disciple it means that until you have information otherwise, stay with those investments which are trending higher and avoid those that are not. While it sounds easy, it can create internal fortitude upheaval and play tricks on your mental state when upwardly trending markets goes through their normal consolidations/corrections.

As investors what we need to realize and accept is that you can’t catch a 20% move in a stock if you are not willing to lose 5-6%. This is often a normal pullback within 20% moves. Sometimes, stocks that pull back 5-6% from your entry won’t recover and you will have to sell them for a loss. That is a part of investing. It’s ok because no one gets them all correct. Being wrong is often not a choice. Staying wrong though always is.

In the same line of thought – you can’t catch a 100% move in a stock if you are not willing to go through a 20% drawdown. Note that I say a drawdown, not a loss. They are two totally different things. If you time your entry properly, you should never let your position drop more than 5-10% below your purchase price. Once your position is profitable and on its way, 10-20% pullbacks are normal. Riding big long-term winners often requires going through deep pullbacks. Not everyone is willing or can stomach a 20% drawdown in individual positions. This is why not everyone can catch and hold 100% movers and why great returns are illusive.

While sticking with the trend sounds simple, the problem is of course, we all know trends eventually end so identifying when that occurs is critical. Since no one can predict the future and we won’t actually know when a trend ends until it can be seen in the rear view mirror (at which point it’s as clear as day) you have to rely on something other than intuition, gut or dart board. In my case, price analysis (my process) tells me when that time is but I also rely on a number of indicators to confirm what I am seeing in price movement. In this blog post I want to highlight one of these indicators I find extremely useful and enlightening and then look at what it is telling us today.

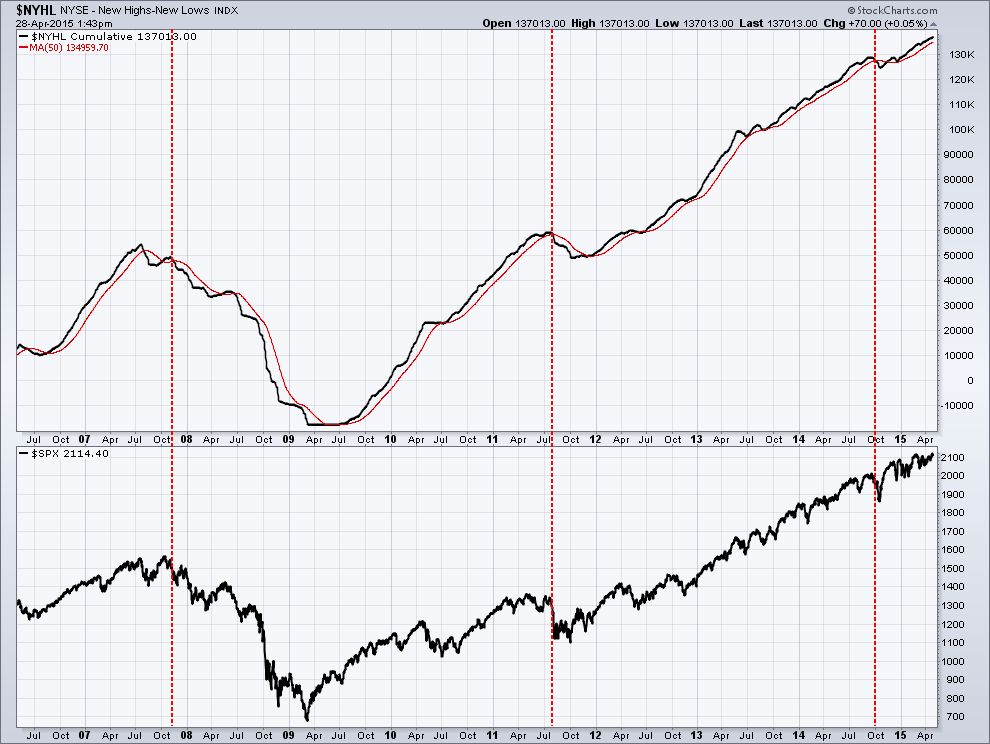

The NYHL is a plot of the number of stocks making new highs subtracting those making new lows (a measurement of market breadth). Intuitively it is pretty obvious the higher the number the stronger the market is. As this number starts to decline it is a sign of market weakness. Below is a 9-year chart of NYHL (upper pane) and the SP500 stock (lower pane). I have applied a 50 day moving average (red line) to the NYHL plot (black line) to use as a signal of market change. A simple, mechanical system to follow would be to reduce exposure to US equities when the NYHL (black line) crosses below the moving average (red line). In the past 9 years that signal has occurred 3 times which I have marked by the red dotted vertical lines. You can see while it is not perfect it does a great job of what it intended to do which is identify points at which a correction is imminent and when an investor should consider reducing risk.

With the markets overly extended and seemly running on fumes struggling to move higher, what is the NYHL telling us right now? Below is the exact same chart as above but only looking at a 2 year time frame allowing us to zoom in for clarity. As you can see the black NYHL line is clearly above the red moving average line which tells us that the current price weakness (as of right now) is just a period of normal consolidation in an ongoing uptrend. Since the trend is our friend and we have nothing telling us otherwise, all pullbacks should be looked at as buying opportunities.

In spite of favorable indicators, a good investor always has their eyes on the market as a reversal can happen at any time. For this reason, now is not the time to become complacent. The Russian proverb President Reagan Russian used in his foreign policy of nuclear disarmament fits nicely in this investment environment, Доверяй, но проверяй, “trust but verify”.

I remember walking into my local grocery store late last year and noticing how the price of a good steak was becoming more expensive than lobster. Beef prices rose on average 30% last year. While it did not touch all-time highs, you had to go back to 2008 before you saw prices that were higher. But like all commodities which are at extremes (high or low), “the market” has a natural built in governor which eventually moderates prices back towards the long term average. Beef prices are another example of when you hear me speak of the power of “reversion to the mean”.

The beauty of technical analysis is that is can be used across any market where historical values are available for analysis and beef fits that bill. In the weekly cattle price chart below we see price hit a peak back in November of last year and created a divergent high (price moved higher while price momentum in the upper pane moved lower) which was the tell-tale warning a decline was imminent. As expected, prices soon fell and eventually bottomed nicely at the prior $74 support line. From there price rebounded higher to create a lower high and form the right shoulder of a potential inverse head and shoulders pattern. In TA there are no absolutes but this pattern is warning of a short term top. If price falls below the $74 neckline the playout of the pattern projects to a $63 target, back to the May 2013 lows.

This is definitely something to keep an eye on because I don’t know about you but I am tired of eating chicken!

Palo Alto Networks (PANW) has been a beast of a stock, doubling in less than a year. It's one of those stocks you wished you owned at the start of its run. As you can see in the chart below, the (red) 50 day moving average has acted as support as each time price fell (albeit briefly) below, it rallied back above it immediately. In the most recent consolidation zone (marked by my two horizontal black lines) price moved sideways for 6 weeks which allowed an unwinding of the overbought conditions and the bulls a rest, touching the 50dma once.

What is compelling about this is today price broke above the upper black horizontal resistance line which it tried but failed to break through 3x prior. In addition, it did it on higher than average volume. This is extremely bullish activity and something a new investor into the stock would look for on an entry point.

As long as the overall market continues to push higher, this stock will likely be a strong beneficiary as all the moving averages are bullishly aligned and momentum is strongly within the bullish range. The upside target for today’s breakout is ~$165. This is a volatile stock and not appropriate for everybody, especially those who don’t have an exit strategy in case the bullish thesis is wrong. Invest safe.

I have written about him many times and posted some of his free work on this blog in the past but this week’s post by Tom McClellan is very enlightening. Tom, one of the fathers of technical analysis, takes on US taxes, US debt, US economy and the US stock market and how they are all interrelated in one fell swoop. I have copied his insightful look below but I encourage anyone who I wants to stay tuned into the market to check in with him regularly here

US Taxes Returning to Economy-Killing Level

The April 15 income tax filing deadline came this week, and so taxes are on the minds of a lot of Americans. As Arthur Laffer noted 3 decades ago, it really is possible to set tax rates too high such that it actually hurts the economy. We appear to be in such a condition now.

I wrote about this topic back in January, when lawmakers were contemplating raising the tax on gasoline. But it is worth revisiting as we see total federal receipts creeping up toward 18% of GDP. Whenever total federal tax receipts have exceeded 18% of GDP, the result has always been a recession for the U.S. economy. And sometimes we can see that effect from a total federal take at less than 18%.

The current number is 17.5%, based on total federal receipts for the 12 months from April 2014 through March 2015, and based on projected GDP for Q1 of 2015. That is very close to the 17.7% reading we saw in 2007, just before the financial market collapse. It is still some distance away from the all-time high reading of 19.8% seen in early 2001, and because of that some economists argue that we can safely go back to those higher levels and have the same strong economy that we saw in the late 1990s.

There are two problems with that hypothesis. The first is that economy of the late 1990s was not as strong as the revisionist historians would like us to believe. The high taxation then pretty effectively killed the technology boom. Total stock listings on the Nasdaq actually peaked in late 1996, and were in a genuine free-fall long before the bubble peak of the Nasdaq Composite Index in 2000. That peak came about because a few large tech stocks were hogging up all of the available liquidity, and crowding out the smaller players, sort of like the biggest hippos taking up the last remaining water hole on the Serengeti during a drought. Unemployment rates also bottomed out in early 2000 and then started upward.

The second problem with that hypothesis is that we don’t have the same demographic conditions now. In 1999, the members of the Baby Boom generation (born 1946 to 1964) were between 35 and 53 years old, in the peak of their entrepreneurial years. They were working hard, building companies, and pushing the economy faster than it would normally go. Now, they are 51 to 69 years old, and are more interested in playing with their grandchildren than in starting a new company and hiring people.

The children of the Baby Boom generation make up what is known as the “Echo Boom”, which peaked in the birth year of 1990. Those 1990 babies are now just 24 to 25 years old, and many are just now moving out from their parents’ homes. So they are not quite at their peak of hard work and entrepreneurialism, and even when they do reach that point, their numbers are just a shadow of their parents’ generation. So the Echo Boomers cannot absorb the same degree of a repressive tax burden that the Baby Boom generation could.

This 18% recession phenomenon is not new. It has worked going all the way back to World War II. Here is the same comparison for the years 1944 to 1980:

![[taxes as percentage of GDP 1944-1980]](https://images.squarespace-cdn.com/content/v1/52fbd83be4b095a0f516b6ea/1429487816502-FLZ9RSHUE3UMAF3V1F05/image-asset.gif)

[taxes as percentage of GDP 1944-1980]

Federal receipts got all the way up to 19.8% of GDP in late 1945, as Congress was trying to pay for WWII and pay off all of those war bonds. And in case anyone fondly remembers the strong war-time economy then, we should remember that an economy which requires price-fixing and rationing is not a strong economy. When people cannot find a place to live because of lumber shortages, and have to grow “Victory Gardens” to have produce, that is not a strong economy. The effects of that taxation repression finally showed up in stock prices during the late 1940s, and only when taxes dropped back down to a less onerous level did the stock market finally start to rebound again.

When the federal government takes a smaller portion of GDP as taxes, that leaves more money in the actual economy for real people to spend on what they want, and to spread around employing other people. Growth is the result. When the federal government takes too much out, it is like a farmer eating his own seed corn; he does not have as much to plant next year.

Meanwhile, federal government spending for the latest 12 months equals 20.4% of GDP, almost 3 percentage points higher than receipts. I keep hoping that someday we will get some leaders who realize that in order to pay off $18 trillion of debt, we have to get the spending number underneath the receipts number, and leave it there for a long time.

And we need to keep the federal receipts number well below 18% if we are to avoid the next recession, and its associated downturn in stock prices. We may already be too late in that regard.