Monday’s 2.4% drop in the SP500 was a punch to the gut for investor’s account but when put into perspective of “worst days” for the index since its inception, it was nothing but an average day at the office.

Lyft Off?

Long term readers know my distaste for buying IPO’s. It’s only because historically those that initially buy an IPO will only make money if they trade it. 99% of investors don’t know how to trade so it usually ends up badly because IPO’s are all about hyping a known company, drawing in the dumb money so the smart money (the initial investors and the bankers bringing them public) can get out. This is why you typically see a ramp up when a company initially goes public and then the stock price comes crashing back to reality. Not always …. but most of the time and the reason to make money on IPO’s, you need trade rather than buy and be a part of the crash.

The better strategy is to wait until the stock price falls back to earth and then buy, assuming it is a company worth my investment capital. The recent IPO, LYFT is a good example of what occurs. The major difference between LYFT and most other IPO’s is LYFT never got the initial buying boost as it peaked on first day of being public and has fallen almost 40% from peak to trough since. This is a rare occurrence for IPO’s but make sense when you consider how over capitalized the company is. Its long-term prospects may be good but a company making no money, has competition everywhere and a market capitalization of more than $20B is, shall I say it, overvalued.

As a for-profit investor it doesn’t mean the stock should be ignored, especially if it presents a price dislocation and is setting up for a potential directional change to the upside like it currently is. Taking a look at the shorter term, 2-hour chart of LYFT below, you can see it has formed an inverse head and shoulder reversal pattern during its recent sideways consolidation. This is a constructive setup if it breaks, holds and confirms above its neckline as it presents an upside target near April 11ths highs, a 15%+ gain.

While I really like this setup as the risk to reward is excellent and as such took a few shares in my trading account early before any breakout occurred, I do want to warn potential followers the company announces earnings next week on 5/7/19. As a general rule I prefer not to hold shares into earnings but will under 2 conditions 1) if I have enough cushion in my entry price to give a high probability of a profit on the investment if poor earnings cause the stock to fall and I get stopped out and 2) if my position size is small enough to ensure a small and contained loss if earnings should cause the stock to fall. Either way its all about risk management.

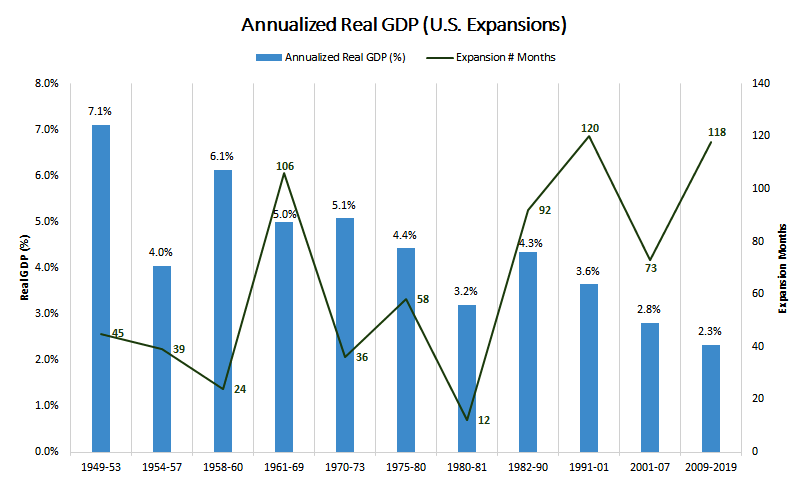

3 More Months? No problem

If we can add another 3 months of economic growth, the US expansion from the 2009 financial crisis bottom will exceed the longest in history. What makes this most interesting is that while it will likely turn out to be the longest expansion, it is on target to also be the weakest in history (annualized GDP)

Investing in Love

As a basic human need, investing in love seems like it would have great possibilities. No matter your age, gender or preferences everyone, at some point or another in their life (sometimes more than once) is “available’ and looking for love. Technological advances make it so much easier now to meet people and avoid the “bar scene”. Match.com, MTCH, is one of those that seems to have caught hold … well, at least the stock has.

Since its IPO in late 2015, MTCH is up more than 300%. As you can see in its chart below, it peaked in Sept of last year, fell more than 40% and has sense come roaring back. Most recent price action has seen the stock breakout from a cup and handle pattern, pointing to a much higher price target above.

It would not be unexpected if MTCH were to back-test the breakout level (rim of the cup) before resuming its climb higher. Those that missed the breakout can look for a great, low risk entry if this were to occur as the risk could be $2 or less with an upside of more than $20, provide a fantastic 10:1 reward to risk opportunity.

A Contrarian Indicator

Here's the theory behind the magazine cover indicator. By the time a something’s success or failure reaches the cover page of a major publication, it is so well known that it is fully known by everyone and those who want to capitalize financially have already done so. For example, once all the good news is out and a company makes the cover of business week, the stock is destined to underperform. The reverse holds for negative stories. It doesn’t have to just be about businesses, it can be about social themes too … remember the 2007-08 housing boom.

An academic study by three finance professors at the University of Richmond put the magazine cover story indicator to the test -- specifically as it focuses on coverage of individual companies. The professors culled headlines from stories in Business Week, Fortune, and Forbes for a 20-year period to examine whether positive cover stories are associated with superior future performance and negative stories are associated with inferior future performance. "Superior" and "inferior" were determined in comparison with an index or another company in the same industry and of the same size.

Here's what the professors found. The research supported the use of magazine cover stories as a contrarian indicator. The most negatively portrayed companies managed to beat the market by an average of 12.4%, whereas the outperformance of the media darlings fell to just 4.2%. The conclusion? Positive stories generally indicate that the stock's price performance has topped out. Negative stories often come right at the time of a turnaround.

The study confirms that it is better to bet against journalists than alongside them. It would be easy to jump to the self-congratulatory conclusion that journalists are incompetent. But that conclusion misses the point. Journalists aren't writing cover stories to make investors money. They are writing cover stories to sell magazines. And "hot topics" sell. But it also means that when a company or financial trend is featured on a magazine cover, the chances are that the trend is already widely known, and universally accepted.

With that in mind, this weeks Business Week cover should raise some eyebrows….

Just because the Government’s measured “version” of inflation, CPI, has been in stall speed for years, doesn’t meant it will always be. Additionally, and most importantly, not everything tracks the inflation rate. Health care is a great example as it has been rising almost 2x the annual “measured” inflation rate. For a what that means over time, take a look, and try not to laugh, at the hospital bill below for what it cost to have a baby in 1958. I think the total bill would be less than the cost than the charge of 2 ibuprofen in today’s medical reality (those that have had a recent surgery can attest to what I say)