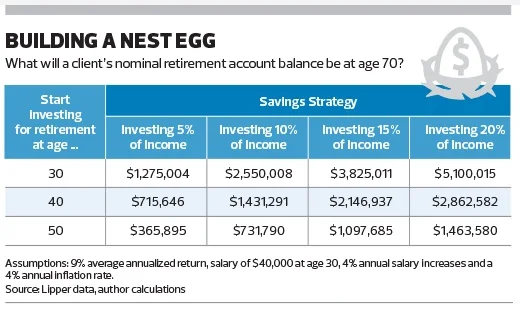

Last week I posted the chart below regarding how much of a nest egg you would accumulate at various savings rates ranging from 5% to 20% and with different start dates for saving, ranging from age 30 to age 50. As was expected, the higher the savings rate and the earlier the start time, the more money you would likely accumulate.

The next logical question would be, once you retire, how long would the money accumulated above last? The following table provides some insight to this.

There are 2 scenarios presented: each assumes a retirement age of 70 and an expense need equal to ~$40,000 in today’s dollars, increased annually by a 4% inflation rate. The first table assumes that you will only use your portfolio to provide half of your expense needs in retirement (as Social Security and other retirement income would be used to provide the other half). The second table assumes you have no other retirement income sources and you must use everything you have saved to provide for your expense needs.

Let’s take the scenario in which a retirement portfolio is expected to provide 50% of the needed retirement income.

There’s an easy rule of thumb here: For each additional decade of retirement income, you should save another 5% chunk — but the correlation is tightest when you start building a portfolio early.

For 30-year-olds, moving to a 10% savings rate from a 5% savings rate provides nine additional years of retirement income. Moving to 15% from 10% adds nine years, and moving to 20% from 15% adds eight years.

In general, adding an additional 5% to your savings rate lengthens the longevity of your retirement portfolio by nearly a decade.

The payoff is less generous for people who start saving later, though. Forty-year-olds who add another 5% savings chunk get about six more years of retirement income, and 50-year-olds who add another 5% savings chunk only get about three more years of retirement income.

In the alternate scenario — with no Social Security, trust, pension or other income, in which the retirement portfolio must provide 100% of the needed retirement income — the savings payoff is lower.

At best, individuals can get five more years of retirement income with each additional 5% chunk of saved income — and that’s if they start saving at age 30. For older savers, each additional 5% chunk of savings gets only two to three years of retirement income; 50-year-olds actually get only one to two years for each additional 5% savings chunk.

We often hear the cliche, “No pain, no gain,” applied to athletic workouts. Yet it is eminently applicable to the process of financial fitness as well — particularly in the context of retirement planning.

The pain is represented by the effort and diligence needed to budget more carefully, which will allow for a higher savings rate. The gain will be a higher ending balance in your retirement portfolio — as well as the development of enhanced budgeting skills, which will be valuable in every season of life. Let the savings begin.