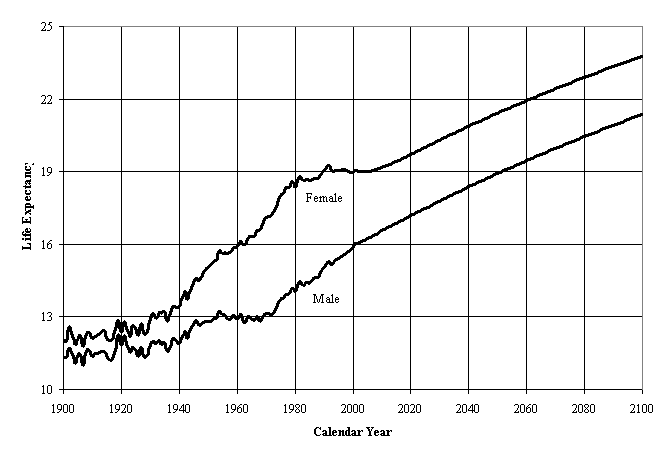

According to Social Security Administration data, Americans have steadily lived longer and longer lives. The chart below shows how many more years, on average, a 65-year-old American has lived since 1900, as well as the expectations that this trend will continue to the end of the current century.

© Social Security Administration Table

For today's seniors, this means most men who reach 65 will live another 17 years, while the average 65 year-old woman will live around 20 more years.

The amazing news is that two decades of retirement -- assuming a retirement age of 65 -- is a lot of time to spend with family, travel, and otherwise pursue passions and activities that may not be compatible with full-time work. But it also requires a significant amount of money to pay for that many years without a steady paycheck. For instance, if you need to generate $50,000 per year in income from your retirement savings, you'd need to have a $1.25 million nest egg, based on the 4% retirement rule (which has flaws, but is a starting point).

The idea of having to save up so much money is daunting. However, there's a big difference between saving $1.25 million and building a $1.25 million portfolio over the long term. For example, if someone started contributing 7% of their salary (with a starting salary of $50,000) in their retirement account at age 25 and invested in a low-cost S&P 500 index fund, they would have a $1.25 million retirement portfolio at age 59, based on the market's historical 10% average rate of return.

The best part? Their total contributions would be around $175,000. That's the power of compound growth over a very long period of time.

The point is, invest -- don't just save -- for retirement. Start as early as possible, and contribute as much as possible.