I thought I would repost an article written last week by Morgan Housel talking about one of the greatest investors, Ed Thorp. For those of you who may not have heard about him, Ed Thorp was the first person to systematically beat casinos at blackjack. He made piles of money, and wrote a book laying out a formula showing how you could do it too.

But not many people did.

Card counting is simple on paper and maddeningly hard in practice. That’s partly because casinos are good at catching card counters. But it’s mostly because even successful card-counting means long, tiring stretches of losing money, which most people can’t stomach.

The casino usually has a 0.5% edge over blackjack players. Thorp’s system titled the stakes, giving players about a 2% edge over the house.

A 2% edge is enough to secure a fortune in the long run. But it also promises hell in the short run, since Thorp was still likely to lose about half his hands. His road to success was paved with agony, as he writes:

I lost steadily, and after four hours I was behind $1,700 and discouraged. Of course, I knew that just as the house can lose in the short run even though it has the advantage in a game, so a card counter can fall behind and this can last for hours or, sometimes, even days. Persisting, I waited for the deck to become favorable just one more time.

The key to Thorp’s system was the ability to survive losing long enough for the 2% edge to materialize. It meant constantly absorbing manageable damage. Many people can’t, or refuse to, do that. Thorp once enlisted a partner, Manny, who was fascinated by the counting system but couldn’t stand the long bouts of losing. “Manny became in turns frantic, disgusted, excited, and finally close to giving up on me as his secret weapon.” As did most who attempted Thorp’s system.

It’s ironic that the secret to winning was learning how to put up with losing, but there it was. “Having an edge and surviving are two different things,” Nassim Taleb once wrote.

This is a great analogy for most business and investing endeavors.

Capitalism doesn’t like edges. It unleashes competition to bang them back toward zero. When edges do arise they’re usually small. A system that gives you a 55%, or 65% chance of success is phenomenal, but it still means you’ll spend close to half your life getting beat up. Since 100% odds of success are either not lucrative, illegal, or ephemeral, the ability to survive losing is a prerequisite to any shot at eventually winning. The business world is a continuous chain of disappointments – recessions, bear markets, brutal competition, employees quitting, supply chain breakdowns, whatever – so every chance at success has to be framed as a net reward down the road amid a constant state of battle and hassle. Thorp understood this. Most of his disciples did not. Most people don’t in general.

Two things come from viewing success as the ability to absorb loss:

It’s easier to be an optimist. Optimism is usually defined as a belief that things will go well. But it’s not. It’s a belief that the odds are in your favor, and over time things will balance out to a favorable outcome even if what happens in between is filled with misery. I’m optimistic about the economy because the odds of success are in its favor. But I still expect a chain of recessions, panics, pullbacks and upheavals. Same for businesses. There are companies whose future I am extremely optimistic about but whose quarterly investor updates I expect to be peppered with setbacks. The two are not mutually exclusive.

You value the margin of safety. Many bets fail not because they were wrong, but because they were mostly right in a situation that required things to be exactly right. Room for error – often called margin of safety – is one of the most underappreciated forces in business. It comes in many forms: A frugal budget, flexible thinking, and a loose timeline – anything that lets you live happily with a range of outcomes. It’s different from being conservative. Conservative is avoiding a certain level of risk. Margin of safety is raising the odds of success at a given level of risk by increasing your chances of survival. Its magic is that the higher your margin of safety, the smaller your edge needs to be to have a favorable outcome. And small edges are where big payoffs tend to live, since most people don’t have the patience to wait around for them.

The point is that short-term loss is usually the cost of admission of long-term gain. It’s a price worth paying, but takes time for the product to be delivered.

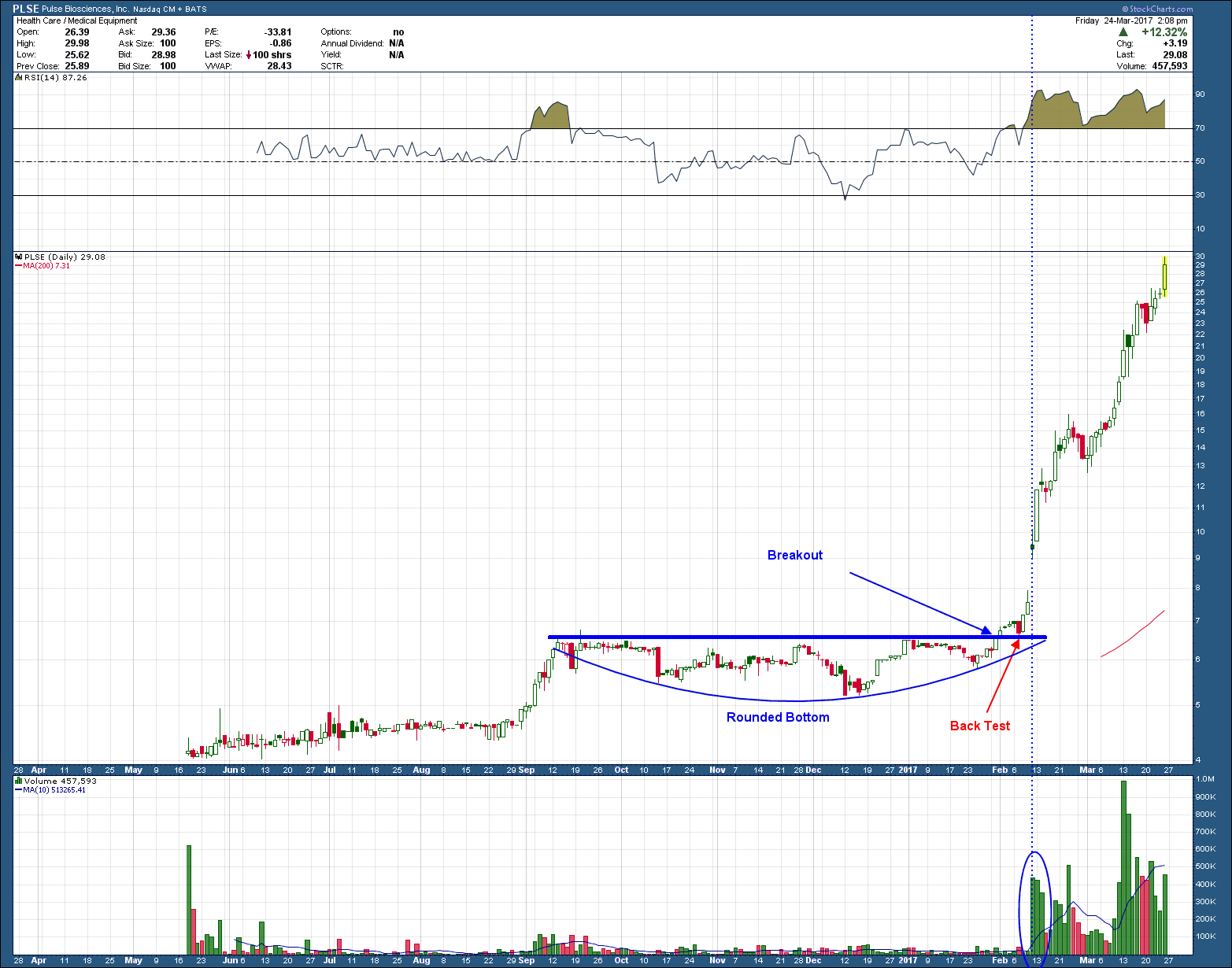

Some may be wondering how this all relates to my investing blog. Besides his casino beating system, his Princeton Newport Partners fund, which was set up in 1969, is recognized as the first quant hedge fund (one that uses algorithms). Over 18 years it turned $1.4m into $273m, compounding at more than double the rate of the S&P 500 without suffering so much as one quarter with a loss. Thorp’s then revolutionary use of mathematics, options-pricing and computers gave him a huge advantage. Ed’s moneymaking abilities have made him the “godfather” of many of today’s greatest investors. The takeaway here is that to be successful at Investing, gambling or any endeavor that puts capital to work in an attempt to profit requires both patience and also an “edge”.